-part-1.jpg)

Volatility returns: Securities lending activity reflects a shifting Q1 market regime

12 May 2026

Matt Chessum, executive director of equity and analytic products at S&P Global Market Intelligence, discusses Q1 across the globe — highlighting standout EMEA equities, leaders across Asia, and record-breaking ETF markets

Image: Shutterstock

Image: Shutterstock

The first quarter of 2026 marked a notable turning point for global financial markets and, by extension, securities lending activity. What began as a continuation of late-2025 optimism, supported by resilient growth, easing inflation and expectations of gradual rate cuts, shifted decisively toward volatility by late February. Geopolitical escalation, rising energy prices, and renewed inflation concerns reshaped investor behaviour across asset classes, creating fertile conditions for securities lending markets globally.

Against this backdrop, securities lending revenues delivered one of the strongest first quarters on record. Elevated volatility, increased dispersion across regions and sectors, and sustained demand for hedging and relative-value strategies all translated into robust activity, particularly across equities, ETFs, and fixed income.

Cash reinvestment strategies became increasingly defensive

During Q1, cash reinvestment strategies within securities lending programmes became increasingly defensive amid heightened rate volatility and central bank recalibration. Earlier policy easing by the Federal Reserve and the Bank of Canada supported front-end liquidity and temporarily anchored overnight and money-market rates, but renewed inflation risks and geopolitical pressures tempered expectations for further near-term cuts.

As US Treasury bill yields and repo rates fluctuated, lenders favoured short-dated, highly liquid reinvestment instruments, prioritising capital preservation, and balance-sheet flexibility over term extension. While absolute cash yields remained attractive, term reinvestment activity softened as programmes sought to avoid locking in rates amid an increasingly uncertain policy outlook heading into Q2. As a result, overall cash reinvestment returns declined when compared with Q4 2025.

Regional equities: Dispersion drives demand

Equity markets experienced a volatile quarter overall, but beneath the headlines sat pronounced regional and sectoral divergence. Rising inflation expectations and higher energy prices weighed on growth-oriented stocks, while value, energy, and materials outperformed.

Regional equities generated approximately US$2.8 billion in revenues during Q1. While this represented a modest decline from the fourth quarter, it remained exceptionally strong by historical standards and marked a significant year-on-year increase.

Americas equities produced US$934 million, the first sub-US$1 billion quarter since Q1 2025 yet still delivered solid year-on-year (YoY) growth. US equity revenues rose five per cent YoY, supported by a sharp rise in balances even as average fees softened. Infosys ADR emerged as the top revenue-generating US equity, highlighting continued demand for offshore technology exposure amid concerns around AI-driven disruption and earnings visibility.

Beyond the US, Canada stood out as the only Americas market to record a YoY revenue decline. Despite strong balance growth, falling average fees weighed on returns. In contrast, Latin America saw robust growth, particularly in Brazil and Mexico, where borrowing responded to rising balances and sector-specific demand, including REITs in Mexico.

EMEA: Specials bring the region back to life

EMEA equities were one of the standout stories of the quarter. Revenues rose 63 per cent YoY, supported by growth in both balances and average fees. Sweden remained the largest contributor, followed by Germany, France, and the UK.

Notably, EMEA equity revenues in Q1 were higher than any quarter in 2025 except Q2, underscoring the structural improvement in regional borrowing dynamics.

Asia: Sustained strength amid volatility

Asian equities delivered another strong quarter, generating US$997 million, marking the third consecutive quarter close to the US$1 billion threshold. This performance was driven by rising balances and resilient fees, even amid increased market volatility.

Taiwan led the region, producing US$240 million in revenues as balances reached record levels and lendable supply nearly doubled YoY. South Korea also saw meaningful growth, with revenues peaking at their highest monthly levels in many years, driven by demand for semiconductor stocks.

Across the wider region, including Hong Kong, Australia, Malaysia, and Singapore, increased activity in mining, technology, and semiconductor names supported revenues. Asian equity balances averaged US$359 billion for the quarter, up 47 per cent YoY, reflecting continued engagement.

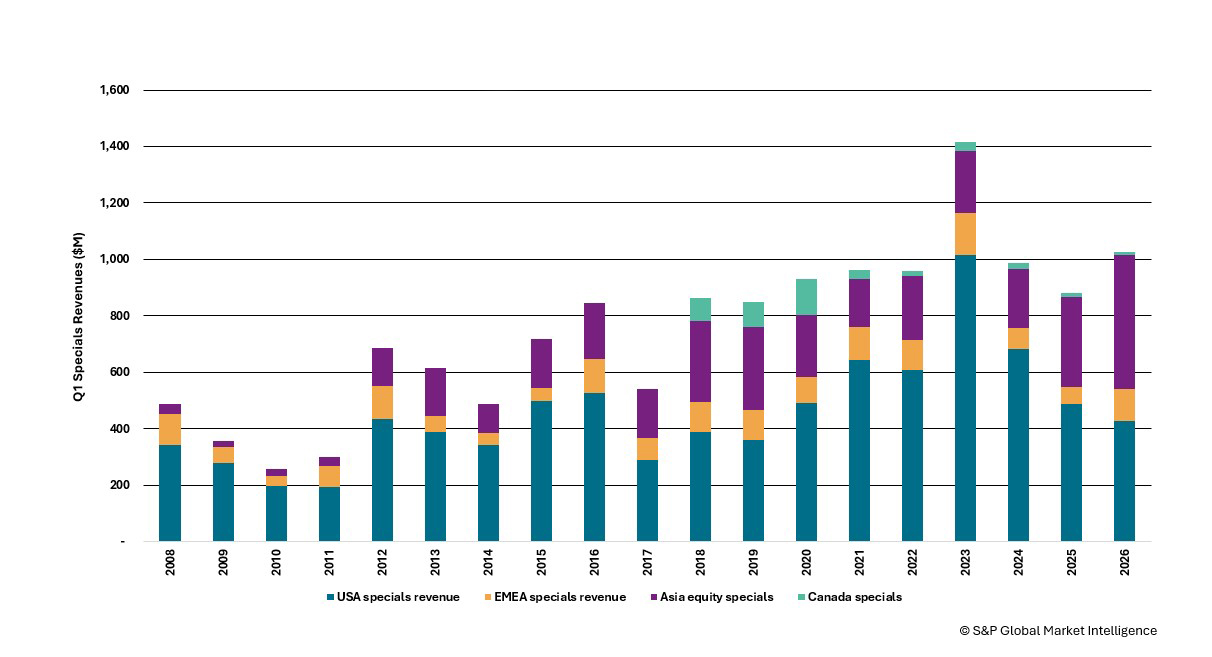

Equity specials: Concentrated but still influential

Equity specials remained a significant contributor, generating US$1.03 billion during Q1, around 36 per cent of total equity revenues. While this was below Q4’s elevated levels, Q1 2026 still marked the second-highest first quarter for specials since 2008.

A notable shift occurred as Asian equity specials overtook the US for the first time in many years. Meanwhile, US and Canadian specials activity was more subdued, reflecting improved liquidity and fewer dislocations earlier in the quarter.

The top 10 revenue-generating equities contributed US$215 million, with software, services, and pharmaceutical names dominating. Once again, Infosys ADR topped the table, reinforcing the theme of technology-related uncertainty driving borrowing demand.

Q1 Equity special revenues

ETFs: Hedging vehicles in high demand

ETF markets experienced a record-breaking start to 2026, with global net inflows reaching approximately US$460 billion during Q1. Securities lending activity mirrored this momentum. ETF lending revenues surged 48 per cent YoY to US$394 million, making it one of the most lucrative quarters on record for the asset class.

Borrowing increased as investors used ETFs for efficient hedging and thematic positioning, particularly during periods of heightened volatility in March. While US-listed ETFs generated the majority of revenues, strong growth was also seen across European and Asian ETFs as balances expanded rapidly.

Demand for leveraged equity ETFs and fixed income products rose sharply as market uncertainty increased. Corporate bond ETFs such as LQD and HYG were among the highest revenue generators, reflecting their role as quick and liquid instruments for expressing credit risk views during a period of widening spreads.

ADRs: Steady contributors

American depository receipt (ADR) lending remained robust, with revenues rising 61 per cent YoY to US$123 million. Higher average fees helped offset slightly lower volumes compared with Q4. Once again, Indian IT ADRs dominated activity, as investors reassessed valuation and earnings risks in the context of accelerating AI investment cycles.

Fixed income: Volatility supports borrowing

Fixed income lending experienced a strong quarter as bond markets repriced around higher-for-longer policy expectations. Government bond revenues rose 27 per cent YoY to US$680 million, an uncommon outcome for a first quarter traditionally marked by lower positioning.

Short-dated government bonds were particularly active as markets shifted away from anticipating swift rate cuts. US Treasuries and French government bonds led activity, with occasional single-issue dislocations driving sharp fee spikes.

Corporate bond lending also strengthened, generating US$274 million, up 12 per cent YoY, as balances reached one of their highest quarterly averages on record. Increased borrowing demand reflected investor repositioning amid widening spreads and growing differentiation between public and private credit markets.

Looking ahead: A supportive backdrop for lending

By the end of Q1, it was clear that markets had entered a new phase defined by geopolitical risk, energy-driven inflation uncertainty, and greater cross-asset volatility. For securities lending, these conditions proved constructive.

Looking into Q2, unresolved geopolitical tensions, evolving AI-related investment dynamics and finely balanced credit markets suggest that demand for hedging, liquidity, and relative-value strategies may remain well supported. Should current volatility persist, securities lending activity across equities, ETFs, and fixed income appears positioned to continue benefiting from an increasingly dynamic market environment.

Against this backdrop, securities lending revenues delivered one of the strongest first quarters on record. Elevated volatility, increased dispersion across regions and sectors, and sustained demand for hedging and relative-value strategies all translated into robust activity, particularly across equities, ETFs, and fixed income.

Cash reinvestment strategies became increasingly defensive

During Q1, cash reinvestment strategies within securities lending programmes became increasingly defensive amid heightened rate volatility and central bank recalibration. Earlier policy easing by the Federal Reserve and the Bank of Canada supported front-end liquidity and temporarily anchored overnight and money-market rates, but renewed inflation risks and geopolitical pressures tempered expectations for further near-term cuts.

As US Treasury bill yields and repo rates fluctuated, lenders favoured short-dated, highly liquid reinvestment instruments, prioritising capital preservation, and balance-sheet flexibility over term extension. While absolute cash yields remained attractive, term reinvestment activity softened as programmes sought to avoid locking in rates amid an increasingly uncertain policy outlook heading into Q2. As a result, overall cash reinvestment returns declined when compared with Q4 2025.

Regional equities: Dispersion drives demand

Equity markets experienced a volatile quarter overall, but beneath the headlines sat pronounced regional and sectoral divergence. Rising inflation expectations and higher energy prices weighed on growth-oriented stocks, while value, energy, and materials outperformed.

Regional equities generated approximately US$2.8 billion in revenues during Q1. While this represented a modest decline from the fourth quarter, it remained exceptionally strong by historical standards and marked a significant year-on-year increase.

Americas equities produced US$934 million, the first sub-US$1 billion quarter since Q1 2025 yet still delivered solid year-on-year (YoY) growth. US equity revenues rose five per cent YoY, supported by a sharp rise in balances even as average fees softened. Infosys ADR emerged as the top revenue-generating US equity, highlighting continued demand for offshore technology exposure amid concerns around AI-driven disruption and earnings visibility.

Beyond the US, Canada stood out as the only Americas market to record a YoY revenue decline. Despite strong balance growth, falling average fees weighed on returns. In contrast, Latin America saw robust growth, particularly in Brazil and Mexico, where borrowing responded to rising balances and sector-specific demand, including REITs in Mexico.

EMEA: Specials bring the region back to life

EMEA equities were one of the standout stories of the quarter. Revenues rose 63 per cent YoY, supported by growth in both balances and average fees. Sweden remained the largest contributor, followed by Germany, France, and the UK.

Notably, EMEA equity revenues in Q1 were higher than any quarter in 2025 except Q2, underscoring the structural improvement in regional borrowing dynamics.

Asia: Sustained strength amid volatility

Asian equities delivered another strong quarter, generating US$997 million, marking the third consecutive quarter close to the US$1 billion threshold. This performance was driven by rising balances and resilient fees, even amid increased market volatility.

Taiwan led the region, producing US$240 million in revenues as balances reached record levels and lendable supply nearly doubled YoY. South Korea also saw meaningful growth, with revenues peaking at their highest monthly levels in many years, driven by demand for semiconductor stocks.

Across the wider region, including Hong Kong, Australia, Malaysia, and Singapore, increased activity in mining, technology, and semiconductor names supported revenues. Asian equity balances averaged US$359 billion for the quarter, up 47 per cent YoY, reflecting continued engagement.

Equity specials: Concentrated but still influential

Equity specials remained a significant contributor, generating US$1.03 billion during Q1, around 36 per cent of total equity revenues. While this was below Q4’s elevated levels, Q1 2026 still marked the second-highest first quarter for specials since 2008.

A notable shift occurred as Asian equity specials overtook the US for the first time in many years. Meanwhile, US and Canadian specials activity was more subdued, reflecting improved liquidity and fewer dislocations earlier in the quarter.

The top 10 revenue-generating equities contributed US$215 million, with software, services, and pharmaceutical names dominating. Once again, Infosys ADR topped the table, reinforcing the theme of technology-related uncertainty driving borrowing demand.

Q1 Equity special revenues

ETFs: Hedging vehicles in high demand

ETF markets experienced a record-breaking start to 2026, with global net inflows reaching approximately US$460 billion during Q1. Securities lending activity mirrored this momentum. ETF lending revenues surged 48 per cent YoY to US$394 million, making it one of the most lucrative quarters on record for the asset class.

Borrowing increased as investors used ETFs for efficient hedging and thematic positioning, particularly during periods of heightened volatility in March. While US-listed ETFs generated the majority of revenues, strong growth was also seen across European and Asian ETFs as balances expanded rapidly.

Demand for leveraged equity ETFs and fixed income products rose sharply as market uncertainty increased. Corporate bond ETFs such as LQD and HYG were among the highest revenue generators, reflecting their role as quick and liquid instruments for expressing credit risk views during a period of widening spreads.

ADRs: Steady contributors

American depository receipt (ADR) lending remained robust, with revenues rising 61 per cent YoY to US$123 million. Higher average fees helped offset slightly lower volumes compared with Q4. Once again, Indian IT ADRs dominated activity, as investors reassessed valuation and earnings risks in the context of accelerating AI investment cycles.

Fixed income: Volatility supports borrowing

Fixed income lending experienced a strong quarter as bond markets repriced around higher-for-longer policy expectations. Government bond revenues rose 27 per cent YoY to US$680 million, an uncommon outcome for a first quarter traditionally marked by lower positioning.

Short-dated government bonds were particularly active as markets shifted away from anticipating swift rate cuts. US Treasuries and French government bonds led activity, with occasional single-issue dislocations driving sharp fee spikes.

Corporate bond lending also strengthened, generating US$274 million, up 12 per cent YoY, as balances reached one of their highest quarterly averages on record. Increased borrowing demand reflected investor repositioning amid widening spreads and growing differentiation between public and private credit markets.

Looking ahead: A supportive backdrop for lending

By the end of Q1, it was clear that markets had entered a new phase defined by geopolitical risk, energy-driven inflation uncertainty, and greater cross-asset volatility. For securities lending, these conditions proved constructive.

Looking into Q2, unresolved geopolitical tensions, evolving AI-related investment dynamics and finely balanced credit markets suggest that demand for hedging, liquidity, and relative-value strategies may remain well supported. Should current volatility persist, securities lending activity across equities, ETFs, and fixed income appears positioned to continue benefiting from an increasingly dynamic market environment.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times