Reading short interest through the lending market, EquiLend

Interview

EquiLend

Reading short interest through the lending market

17 February 2026

Nancy Allen, head of Data & Analytics Solutions at EquiLend, introduces the firm’s new daily Predicted Short Interest, designed to give an AI‑derived view of current short exposure

Image: Nancy Allen

Investment professionals across the global markets are well-aware of the limitations of traditional US short‑interest data: it provides a backward‑looking snapshot that arrives only after market conditions have already shifted. By the time the figures are released, positions have changed, risk has been reassessed, and teams have executed on important decisions without accurate knowledge of short activity.

Those days are over. EquiLend is pleased to introduce our new daily Predicted Short Interest, calculated using a machine learning model and designed to provide an AI‑derived view of current short exposure. With this enhancement, the market no longer needs to wait for reported short‑interest figures to gauge sentiment in a stock. The model filters out the noise traditionally found in securities finance on-loan balances, which have long been used, somewhat imperfectly, as an indication of short interest.

Within our securities finance data set, borrow requests, new loans, returns, recalls, and inventory movements generate a high-frequency stream of signals that reflect how short positions form and unwind. The machine-learning model imposes structure on that flow, separating directional short demand from the mechanics of financing, settlement, and liquidity management. The edge comes from knowing when borrowing activity reflects a real change in positioning — and when it is simply noise.

When borrow data is on the money

In hard‑to‑borrow names, the relationship between borrowing activity and short interest is often quite direct. When an investor initiates a short, a loan is triggered in the securities finance markets and is relatively quickly reflected in utilisation, borrow balances, and pricing. When demand rises, it becomes visible almost immediately.

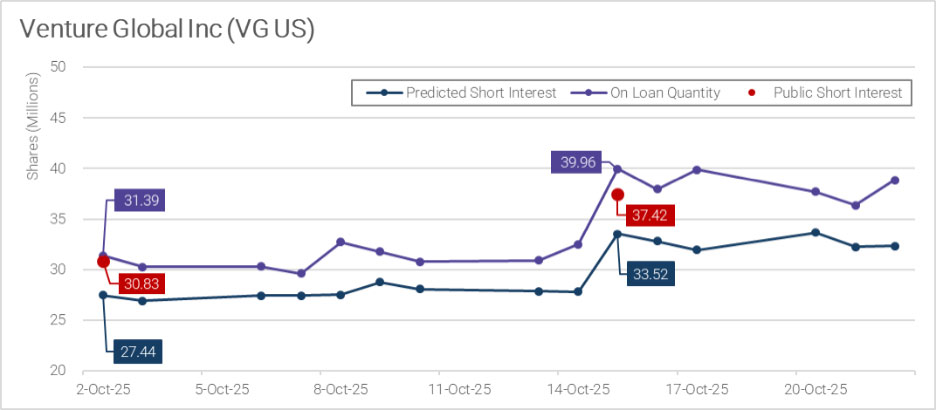

Venture Global offers a useful example. After the company lost a US$1 billion arbitration case against BP on 10 October, the stock declined sharply. In the days that followed, lending desks observed a steady increase in borrow balances as short exposure built alongside the volatility. When the exchange‑reported short‑interest data was later released, it simply confirmed what the lending market had already been signaling.

Venture Global

For investors monitoring daily and intraday loan data, the dynamics in this case are straightforward. Borrow demand increased, availability tightened, and short exposure rose accordingly. In situations like this, lending data behaves exactly as practitioners would expect.

When borrow data needs a second look

The picture becomes more nuanced in easy-to-borrow and general collateral names. In these cases, brokers can often source stock internally, so changes in short positioning are not always mirrored by changes in borrow balances.

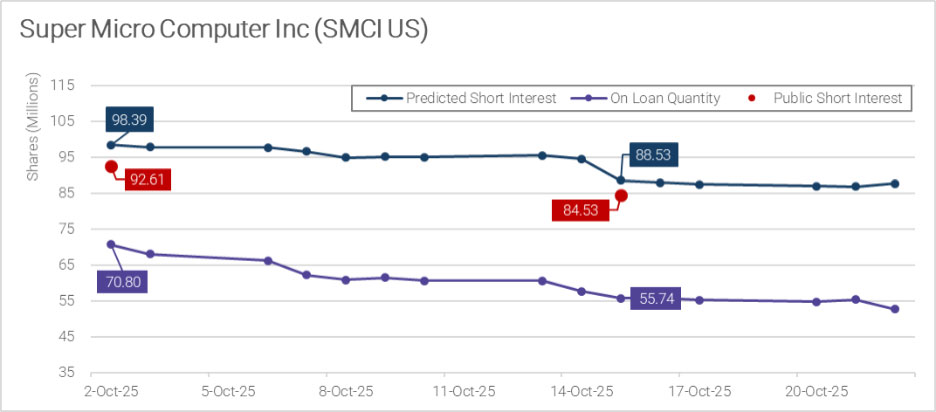

Super Micro Computer illustrates this well. In October 2025, the stock faced significant shorting pressure, yet it remained easy to source from a lending perspective. Utilisation held in the 25 to 35 per cent range, and borrow costs stayed low. As the stock rallied, short sellers reduced exposure, and loan balances dropped by roughly eight million shares.

Super Micro Computer

The direction was right — short interest was coming down — but the raw borrow data overstated the magnitude of the move. EquiLend’s new predictive model adjusted for internalisation and non-directional flows, pointing to a more modest decline that later proved closer to the exchange-reported figures. It is a useful reminder that in liquid names, borrow data alone can exaggerate activity.

Borrowing does not always mean shorting

Another challenge is separating short activity from borrows driven by other purposes which may include settlement coverage, financing trades, or balance sheet management.

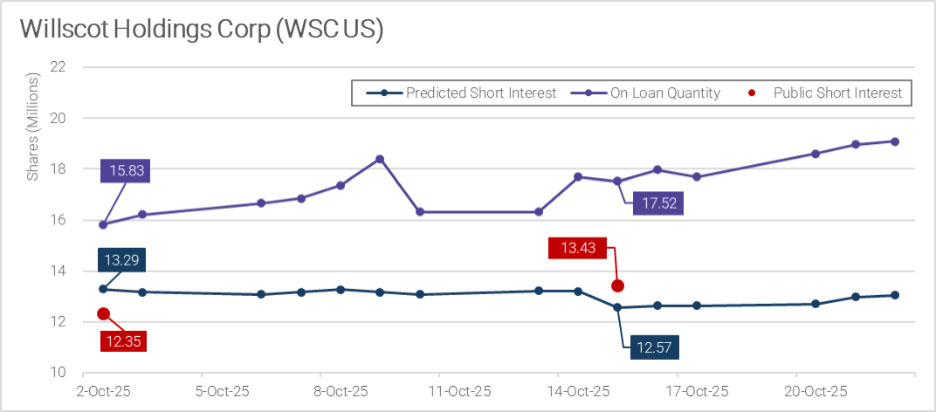

WillScot Holdings is a clear example. Despite ongoing negative sentiment, borrowed shares consistently averaged well above the reported short interest. In October 2025, borrow balances fluctuated, while published short interest remained relatively flat.

Willscot Holdings Corp

While the lending market was active in WSC, not all new loans reflected new bearish conviction. Once non‑directional lending flows were filtered out, a much steadier picture of short exposure emerged — one that lined up more closely with what ultimately appeared in public data.

What this means for investors

For those who live and breathe securities finance, none of the above should be surprising. Borrow data has always been an early signal — it simply delivers the best value when viewed through the right lens.

In tight names, shifts in borrow demand often tell the short interest story quickly. In liquid names, internalisation and routine lending flows need to be considered. And in names with heavy financing activity, borrow balances may say more about balance sheet strategy than directional positioning.

That is exactly where AI‑derived short interest changes the game and distinguishes signal from noise. EquiLend’s Predicted Short Interest, now available via API, is designed to be easily integrated into workflows including trading algorithms and risk models to deliver clarity where traditional metrics fall short.

Predicted Short Interest elevates borrow data from a rough proxy to a precise, decision‑ready metric. It reveals true positioning, adds essential context, and provides decision makers with a clearer, real-time analysis of market sentiment. In an environment where speed and accuracy drive performance, that level of insight is not just helpful — it is a meaningful competitive advantage.

NO FEE, NO RISK 100% ON RETURNSIf you invest in only one securities finance news source this

year, make sure it is your free subscription to Securities Finance Times

Image: Nancy Allen

Image: Nancy Allen