Matthew Chessum, director of securities finance at S&P Global Market Intelligence, describes a perfect storm for the property sector as challenging trading conditions drive interest from short sellers

As interest rates have continued to climb over the last 12 to 18 months, so has short interest across the property sector. The increase in interest rates has reduced potential buyers’ purchasing power, while simultaneously increasing the risk-free rate of return for investors. Office space remains underutilised and companies are looking to downsize to reduce costs, following the working-from-home revolution that was adopted during COVID.

A shift to online shopping throughout the pandemic has also decreased demand for commercial real estate as retailers continue to adjust their commercial strategies. The effects of this have recently been felt in the US, with a decline in year-over-year (YoY) sales pushing share prices for some of the most popular US department stores lower. The current situation appears to have created the perfect storm for the property sector, with more challenging trading conditions and lower share price valuations taking hold. In a recent economic survey by a large US bank, real estate was voted by 49 per cent of survey participants to be the most likely source of the next “systemic credit” event.

Pressure on REITs

This sentiment is currently being reflected across securities finance data sets. Real estate investment trusts (REITs) in particular have generated significant interest from borrowers and continue to be the most shorted sector across global equities. As interest and occupancy rates have been popular headlines throughout the post-COVID period, REIT stock prices have been trading at around 20 to 30 per cent below their net asset values.

Currently, across global equities, short loan value as a percentage of market capitalisation stands at 1.57 per cent. To put this in context, financial services is the second most shorted sector globally and short loan value as a percentage of market capitalisation stands at 80bps — nearly half as much as REITs. Short interest across the REIT sector appears to be concentrated across the Americas and Europe. In the US, REITs are the second most shorted sector, just behind financial services.

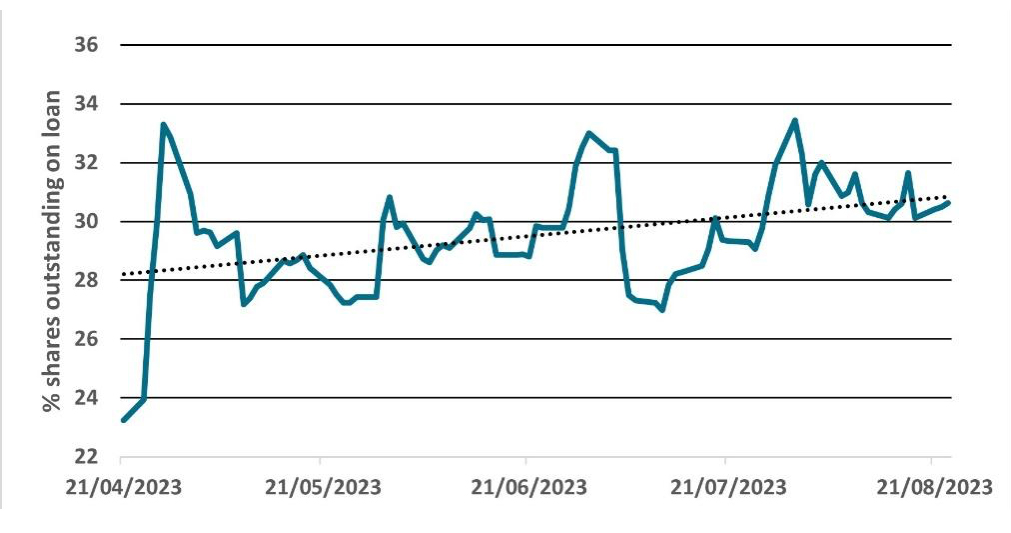

Despite a recent rise in the share price, SL Green Realty Corp (SLG) is currently the most shorted REIT across US equities with 30.63 per cent of its outstanding shares on loan. This company is responsible for acquiring, managing and maximising the value of Manhattan commercial properties. The property sector remains an important indicator of the New York State’s economic activity as commercial rents and commerce provide both revenues and jobs for the State treasury. In the US in particular, the property sector also remains exposed to potential refinancing difficulties as the US banking sector continues to consolidate after the collapse of three regional lenders earlier this year.

Fig 1: Percentage of Shares Outstanding on Loan - SL Green Realty Corp

Across Europe, real estate management and development continues to be the most shorted sector. The property sector across Europe remains impacted by many of the issues facing the REITs in the US — high interest rates, an increase in online shopping and lower office occupancy rates. Long time special Samhallsbyggnadsbolaget I Norden AB (SBB B) remains the most borrowed property stock across the EMEA region, with 24.17 per cent of its outstanding shares on loan. Utilisation in the stock remains high at 95.38 per cent. Peach Property Group AG (PEAN), the Swiss property group, has also become more expensive to borrow over the past few months as demand for the stock has increased. Currently, this stock has 11.08 per cent of its outstanding shares on loan, is showing a utilisation of 81.46 per cent and is the second most-expensive property stock to borrow across the EMEA region.

Across the APAC region, short interest continues to grow across the Asian property sector, despite the property sector not even appearing within the top 10 most-shorted sectors. Falling housing sales across the continent continue to put pressure on property stocks. Asian property companies that remain heavily dependent on mainland China have recently started to show signs of stress, as the decline in economic activity and the country’s weakening economy add to the long list of potential problems that property companies currently face. Historically, mainland China has depended upon its property industry to help fuel its economic growth, accounting for approximately a quarter of the country’s economic output.

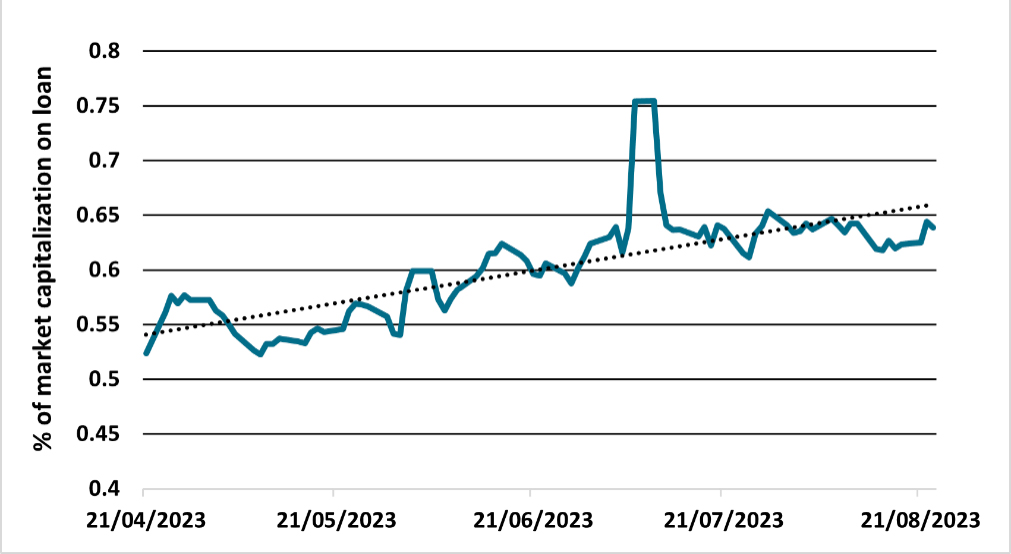

Given the recent softening in economic data and increased chatter of central government stimulus, distressed developers in the region are once again coming under pressure from short sellers. The percentage of market capitalisation on loan across the Asian property sector has been rising steadily since April this year, reaching a recent high of 0.75 per cent at the beginning of July (fig 2).

Fig 2: Asia Real Estate Management and Development

Country Gardens Co Ltd (2007) has sparked particular interest over the past few weeks, as the company missed an interest payment on its bonds and reportedly pulled its latest attempt to raise US$300 million via a share offering in Hong Kong. Country Garden Holdings Co Ltd (2007) continues to be the most heavily borrowed stock within the sector as it faces US$2.9 billion of debt repayments for the rest of the year, weighing heavily on its ability to retain liquidity and meet payment deadlines.

Average borrowing fees continue to move higher as active utilisation surpasses 90 per cent and the percentage of shares outstanding on loan in the company surpasses 8.5 per cent of the free float. Even though the People’s Bank of China has agreed to extend outstanding loans across the sector, financial markets remain cautious of the sector's ability to manage its heavy debt burden while retaining the ability to generate value for investors.

As global economies start to react to the prospect of higher rates for longer, and the world recalibrates following one of the largest and most profound economic shocks ever experienced throughout the recent pandemic, the prospects for the property sector may appear bleak. Despite this, given the fall in share prices, some consolidation has taken place throughout the sector, strengthening companies’ balance sheets and leading to opportunities for investors. As far as short sellers are concerned, however, the property sector remains a firm favourite.