US Treasury clearing evolution: The road to ‘done-away’

11 March 2026

Richard Gallagher, head of sales and client management, Asia Pacific, Financing Solutions, State Street Markets, examines the upcoming US Treasury clearing mandate in the US and how this is shaping the priorities of APAC global investors

Image: stock.adobe.com/rey

Image: stock.adobe.com/rey

US Treasuries (UST) sit at the core of the global financial system, underpinning liquidity, risk-free pricing, and collateral transformation across markets.

On 13 December 2023, the Securities and Exchange Commission (SEC) mandated all trades of US debt securities to be centrally cleared. The mandate represents one of the most significant structural changes to the UST market in decades, expanding central clearing well beyond its traditional scope. As implementation timelines approach, the focus for global investors — particularly in Asia Pacific — has shifted from ‘whether to clear’ to ‘how clearing can be achieved without sacrificing execution flexibility, liquidity access, or operating efficiency’.

This evolution is accelerating new access models, the emergence of a multi-covered clearing agency (CCA) landscape, and a decisive move toward the ‘done-away’ execution model.

FICC foundations: Mandate, scale, and market evolution

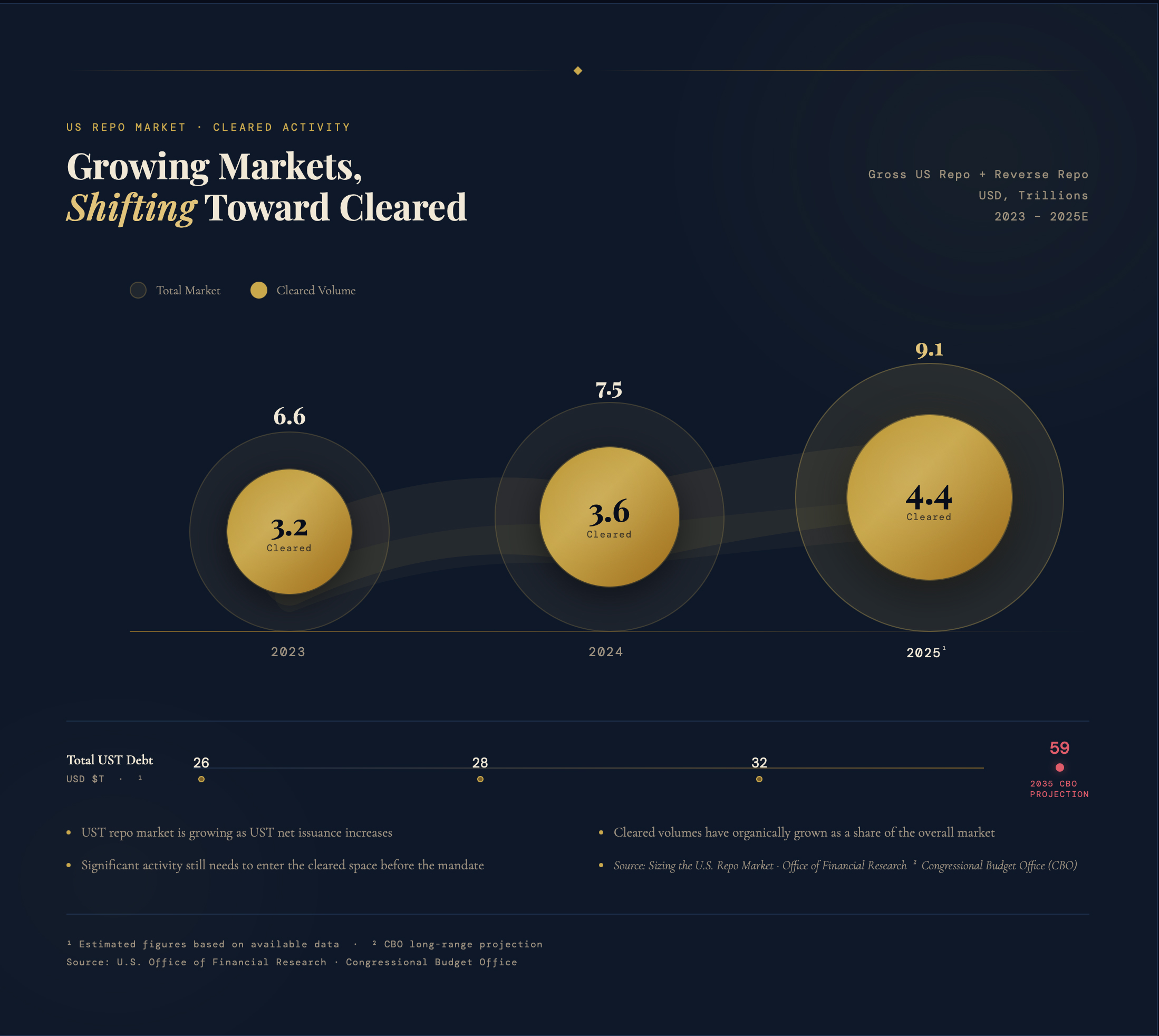

The SEC’s expanded UST clearing mandate represents one of the most significant structural reforms to global fixed-income markets in decades. The rule requires that a substantially larger proportion of secondary-market UST cash and repo transactions be centrally cleared through SEC-designated CCAs. Under the mandate’s current timeline, cash transactions must comply by 31 December 2026, with repo transactions following by 30 June 2027.

At the centre of this framework sits the Fixed Income Clearing Corporation (FICC), the incumbent CCA for UST repo. Even prior to the mandate, central clearing was gaining momentum as dealers faced balance-sheet constraints and funding volatility highlighted the benefits of netting, standardised risk management, and default mutualisation.

Recent liquidity stresses have reinforced these dynamics. Episodes such as the September 2019 repo market cash crunch, Covid-19 dislocation, the April 2025 funding-market imbalance, and various auction-related tensions all demonstrated how quickly liquidity can fragment in bilateral markets. By contrast, expanding the share of activity cleared through FICC is expected to reduce systemic vulnerabilities by consolidating risk management, mutualising default protections, and strengthening market resilience — helping to limit the likelihood and severity of such disruptions in the future.

Clearing volumes have already begun to scale. Mandate materials show the cleared share of UST repo rising steadily, while sponsored clearing volumes continue to expand, reaching approximately US$2.96 trillion at year-end. This growth underscores how clearing infrastructure becomes increasingly central during periods of balance-sheet sensitivity and market stress.

Against this backdrop, the evolution from FICC’s Sponsored Member Repo (SMR) to Agent Clearing Service (ACS) reflects increasing standardisation and flexibility rather than replacement of one model by another. While SMR provides an important access path into cleared repo, ACS was introduced to better align UST clearing with established futures commission merchant (FCM)-style client clearing frameworks and to help promote broader adoption of done-away structures at scale.

The facts: Asia’s structural importance to the UST market

Asia’s relevance to the UST market is not anecdotal — it is quantifiable. Japan holds roughly 12.4 per cent and China around 8.9 per cent of total foreign ownership of US publicly-held federal debt, placing both among the largest foreign holders globally. In aggregate, Asian investors hold approximately 40–45 per cent of offshore US debt instruments.

These holdings play a foundational role in reserve management, liquidity provision, and collateral transformation across APAC. As UST market structure evolves, the transmission effects extend directly to Asian asset managers, hedge funds, pension funds, and central bank-related institutions that rely on UST for funding and risk management.

On the clearing side, data illustrates quantifiable momentum. The proportion of centrally cleared UST repo activity has increased materially over the past two years, rising from roughly 15 per cent in early 2023 to more than 30 per cent by early 2025. Crucially, a significant volume of repo remains uncleared and must migrate before the mandate’s repo compliance deadline, elevating clearing access and capacity from an operational concern to a strategic imperative.

Within this expanding cleared ecosystem, large global clearing agents play a central role in supporting sponsored and agented access to FICC-cleared repo markets. State Street accounts for an estimated 20–30 per cent of cleared reverse repo activity and roughly 10–15 per cent of total sponsored cleared volumes, underscoring the scale and infrastructure required to support the market’s transition.

Clearing models: From sponsored repo to agented flexibility

The industry’s first scalable response to expanded clearing was the SMR model. Under this ‘done-with’ model, buy side firms execute and clear trades through a sponsoring dealer that submits transactions to FICC and guarantees client performance. For many APAC investors, SMR remains the foundation of cleared repo activity, offering operational simplicity and access to central counterparty (CCP) protections without the burden of direct membership.

As clearing volumes increase and investment strategies diversify, greater flexibility in how execution and clearing are combined has become increasingly important. FICC’s ACS model extends the sponsored framework by standardising agented clearing workflows. In practice, implementations can vary by provider, supporting done-with clearing only or a combination of done-with and done-away structures.

However, the most significant evolution lies in the ability to support true done-away clearing at scale. Under SMR, the client effectively becomes a quasi-member of FICC — becoming subject to certain rulebook provisions and typically required to be domiciled in jurisdictions acceptable to FICC — so operational, legal, and jurisdictional considerations can be more involved.

By contrast, under ACS the client does not become an FICC member; FICC views the activity as a clearing agent on behalf of the client. This structure is lower-touch from the client’s perspective, enabling investors to execute with a broad network of bilateral counterparties while routing trades to a single clearing agent for novation. In practice, this preserves long-standing dealer relationships, expands access to liquidity across time zones, and avoids the operational and legal complexity associated with maintaining multiple clearing memberships.

CCAs and CCPs: The emergence of a multi-CCA ecosystem

The evolution of access models is unfolding alongside a broader transformation in clearing infrastructure itself. In addition to FICC, the SEC’s approval of Chicago Mercantile Exchange Securities Clearing (CMESC) in December 2025 introduces complementary clearing capacity into the UST market, with go-live expected in 2026.

In practice, the initial scaling of new CCAs is likely to be gradual. Capital efficiencies achieved through trading across multiple CCAs may influence how firms manage activity, particularly around balance sheet reporting dates, but onboarding, liquidity concentration, and operational readiness will shape early adoption.

CME’s offering is positioned to coexist alongside incumbent infrastructure, with a particular emphasis on portfolio-based margin efficiencies for participants active across UST cash, repo, futures, and options. Other CCPs, including Intercontinental Exchange (ICE) and London Clearing House (LCH), have publicly signaled intent to enter the UST clearing space. While ICE has submitted an application to the SEC, formal approval is still expected to take time, reinforcing that a multi-CCA future will emerge progressively rather than overnight.

It is critical to distinguish CCAs from access models. Sponsored and agent clearing do not replace CCPs; they provide pathways into clearing infrastructure. This distinction becomes increasingly important as participants evaluate long-term clearing strategies in a multi-CCA environment. For example, cross-product margining could offer significant enhancement and differentiation to the current offering in the market.

What APAC clients are demanding and the end-state market

For APAC investors, the core message is consistent and pragmatic: achieve clearing compliance while preserving bilateral execution flexibility. Many institutions have spent decades cultivating diversified dealer relationships to manage liquidity, pricing, and risk across market conditions, and increasingly require in-region access to UST repo markets — particularly the ability to source pricing, market colour and execution liquidity during APAC hours, often ahead of the US trading hours.

Done-away clearing directly addresses this requirement. By separating execution choice from clearing obligation, it allows investors to retain counterparty diversification while centralising clearing through a single agent, preserving access to broad dealer liquidity while improving operational efficiency. For investors in APAC, however, execution flexibility alone is not sufficient. Clients are also seeking margin visibility and notification during APAC business hours, alongside documentation frameworks that better reflect regional market conventions.

In this emerging landscape, the ability to support multiple access models at scale and with genuine regional depth becomes critical. As one of the largest clearing providers globally, State Street is already well-positioned within the cleared UST ecosystem to support this transition — combining APAC coverage with experience across sponsored and agent clearing models, and the operational capability to support margining, documentation, and execution workflows aligned with local market expectations in a multi-CCA environment.

The future state of the UST market is therefore one of structured flexibility: multiple CCAs, interoperable access models, and preserved execution choice, underpinned by centralised risk management and globally coordinated operations. In that future, done-away clearing is not a niche solution — it is the logical destination of the UST clearing evolution for globally active APAC institutions.

Figure 1

Figure 2

Figure 3

Figure 4

On 13 December 2023, the Securities and Exchange Commission (SEC) mandated all trades of US debt securities to be centrally cleared. The mandate represents one of the most significant structural changes to the UST market in decades, expanding central clearing well beyond its traditional scope. As implementation timelines approach, the focus for global investors — particularly in Asia Pacific — has shifted from ‘whether to clear’ to ‘how clearing can be achieved without sacrificing execution flexibility, liquidity access, or operating efficiency’.

This evolution is accelerating new access models, the emergence of a multi-covered clearing agency (CCA) landscape, and a decisive move toward the ‘done-away’ execution model.

FICC foundations: Mandate, scale, and market evolution

The SEC’s expanded UST clearing mandate represents one of the most significant structural reforms to global fixed-income markets in decades. The rule requires that a substantially larger proportion of secondary-market UST cash and repo transactions be centrally cleared through SEC-designated CCAs. Under the mandate’s current timeline, cash transactions must comply by 31 December 2026, with repo transactions following by 30 June 2027.

At the centre of this framework sits the Fixed Income Clearing Corporation (FICC), the incumbent CCA for UST repo. Even prior to the mandate, central clearing was gaining momentum as dealers faced balance-sheet constraints and funding volatility highlighted the benefits of netting, standardised risk management, and default mutualisation.

Recent liquidity stresses have reinforced these dynamics. Episodes such as the September 2019 repo market cash crunch, Covid-19 dislocation, the April 2025 funding-market imbalance, and various auction-related tensions all demonstrated how quickly liquidity can fragment in bilateral markets. By contrast, expanding the share of activity cleared through FICC is expected to reduce systemic vulnerabilities by consolidating risk management, mutualising default protections, and strengthening market resilience — helping to limit the likelihood and severity of such disruptions in the future.

Clearing volumes have already begun to scale. Mandate materials show the cleared share of UST repo rising steadily, while sponsored clearing volumes continue to expand, reaching approximately US$2.96 trillion at year-end. This growth underscores how clearing infrastructure becomes increasingly central during periods of balance-sheet sensitivity and market stress.

Against this backdrop, the evolution from FICC’s Sponsored Member Repo (SMR) to Agent Clearing Service (ACS) reflects increasing standardisation and flexibility rather than replacement of one model by another. While SMR provides an important access path into cleared repo, ACS was introduced to better align UST clearing with established futures commission merchant (FCM)-style client clearing frameworks and to help promote broader adoption of done-away structures at scale.

The facts: Asia’s structural importance to the UST market

Asia’s relevance to the UST market is not anecdotal — it is quantifiable. Japan holds roughly 12.4 per cent and China around 8.9 per cent of total foreign ownership of US publicly-held federal debt, placing both among the largest foreign holders globally. In aggregate, Asian investors hold approximately 40–45 per cent of offshore US debt instruments.

These holdings play a foundational role in reserve management, liquidity provision, and collateral transformation across APAC. As UST market structure evolves, the transmission effects extend directly to Asian asset managers, hedge funds, pension funds, and central bank-related institutions that rely on UST for funding and risk management.

On the clearing side, data illustrates quantifiable momentum. The proportion of centrally cleared UST repo activity has increased materially over the past two years, rising from roughly 15 per cent in early 2023 to more than 30 per cent by early 2025. Crucially, a significant volume of repo remains uncleared and must migrate before the mandate’s repo compliance deadline, elevating clearing access and capacity from an operational concern to a strategic imperative.

Within this expanding cleared ecosystem, large global clearing agents play a central role in supporting sponsored and agented access to FICC-cleared repo markets. State Street accounts for an estimated 20–30 per cent of cleared reverse repo activity and roughly 10–15 per cent of total sponsored cleared volumes, underscoring the scale and infrastructure required to support the market’s transition.

Clearing models: From sponsored repo to agented flexibility

The industry’s first scalable response to expanded clearing was the SMR model. Under this ‘done-with’ model, buy side firms execute and clear trades through a sponsoring dealer that submits transactions to FICC and guarantees client performance. For many APAC investors, SMR remains the foundation of cleared repo activity, offering operational simplicity and access to central counterparty (CCP) protections without the burden of direct membership.

As clearing volumes increase and investment strategies diversify, greater flexibility in how execution and clearing are combined has become increasingly important. FICC’s ACS model extends the sponsored framework by standardising agented clearing workflows. In practice, implementations can vary by provider, supporting done-with clearing only or a combination of done-with and done-away structures.

However, the most significant evolution lies in the ability to support true done-away clearing at scale. Under SMR, the client effectively becomes a quasi-member of FICC — becoming subject to certain rulebook provisions and typically required to be domiciled in jurisdictions acceptable to FICC — so operational, legal, and jurisdictional considerations can be more involved.

By contrast, under ACS the client does not become an FICC member; FICC views the activity as a clearing agent on behalf of the client. This structure is lower-touch from the client’s perspective, enabling investors to execute with a broad network of bilateral counterparties while routing trades to a single clearing agent for novation. In practice, this preserves long-standing dealer relationships, expands access to liquidity across time zones, and avoids the operational and legal complexity associated with maintaining multiple clearing memberships.

CCAs and CCPs: The emergence of a multi-CCA ecosystem

The evolution of access models is unfolding alongside a broader transformation in clearing infrastructure itself. In addition to FICC, the SEC’s approval of Chicago Mercantile Exchange Securities Clearing (CMESC) in December 2025 introduces complementary clearing capacity into the UST market, with go-live expected in 2026.

In practice, the initial scaling of new CCAs is likely to be gradual. Capital efficiencies achieved through trading across multiple CCAs may influence how firms manage activity, particularly around balance sheet reporting dates, but onboarding, liquidity concentration, and operational readiness will shape early adoption.

CME’s offering is positioned to coexist alongside incumbent infrastructure, with a particular emphasis on portfolio-based margin efficiencies for participants active across UST cash, repo, futures, and options. Other CCPs, including Intercontinental Exchange (ICE) and London Clearing House (LCH), have publicly signaled intent to enter the UST clearing space. While ICE has submitted an application to the SEC, formal approval is still expected to take time, reinforcing that a multi-CCA future will emerge progressively rather than overnight.

It is critical to distinguish CCAs from access models. Sponsored and agent clearing do not replace CCPs; they provide pathways into clearing infrastructure. This distinction becomes increasingly important as participants evaluate long-term clearing strategies in a multi-CCA environment. For example, cross-product margining could offer significant enhancement and differentiation to the current offering in the market.

What APAC clients are demanding and the end-state market

For APAC investors, the core message is consistent and pragmatic: achieve clearing compliance while preserving bilateral execution flexibility. Many institutions have spent decades cultivating diversified dealer relationships to manage liquidity, pricing, and risk across market conditions, and increasingly require in-region access to UST repo markets — particularly the ability to source pricing, market colour and execution liquidity during APAC hours, often ahead of the US trading hours.

Done-away clearing directly addresses this requirement. By separating execution choice from clearing obligation, it allows investors to retain counterparty diversification while centralising clearing through a single agent, preserving access to broad dealer liquidity while improving operational efficiency. For investors in APAC, however, execution flexibility alone is not sufficient. Clients are also seeking margin visibility and notification during APAC business hours, alongside documentation frameworks that better reflect regional market conventions.

In this emerging landscape, the ability to support multiple access models at scale and with genuine regional depth becomes critical. As one of the largest clearing providers globally, State Street is already well-positioned within the cleared UST ecosystem to support this transition — combining APAC coverage with experience across sponsored and agent clearing models, and the operational capability to support margining, documentation, and execution workflows aligned with local market expectations in a multi-CCA environment.

The future state of the UST market is therefore one of structured flexibility: multiple CCAs, interoperable access models, and preserved execution choice, underpinned by centralised risk management and globally coordinated operations. In that future, done-away clearing is not a niche solution — it is the logical destination of the UST clearing evolution for globally active APAC institutions.

Figure 1

Figure 2

Figure 3

Figure 4

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times