The next liquidity crisis will not be the one you expect

14 April 2026

In the second instalment of this ongoing series, Cyril Louchtchay de Fleurian, head of securities finance and balance sheet strategy at Capteo: Strategy & Management Consulting, reviews the next potential liquidity crises and how shifts in the market are contributing to unusable liquidity

Image: stock.adobe.com/MediaRaw

Image: stock.adobe.com/MediaRaw

Liquidity is there — until it is no longer executable.

The liquidity regime has changed; recent crises have made that clear. Their defining feature is heterogeneity: the message is constant, the path is not. Liquidity no longer fades in a gradual, readable way — it gaps, withdraws in blocks, fragments, and reconfigures itself across channels that do not necessarily align.

What was once treated as a stable stock to protect now operates under a different logic: an execution capacity — reversible, conditional, and prone to seize up under uncontrolled margin calls, widening spreads, or collapsing roll-over rates. Liquidity no longer fails as a stock; it fails in execution.

The prevailing analytical framework now rests on an untenable fiction: that a liquidity crisis is a rare, systemic event, primarily driven by a lack of volume, and sufficiently homogeneous to be captured by a handful of prudential metrics. Recent episodes have invalidated this view.

Shocks can be exogenous, endogenous, or structural. Breaking points may emerge in markets, balance sheets, collateral, confidence, or geopolitics. Stress then propagates through spreads, haircuts, eligibility, infrastructure constraints, withdrawal behaviour, or deleveraging loops. Crucially, time dynamics diverge sharply: some crises strike suddenly, others erode the market gradually, while others accelerate through self-reinforcing feedback loops. This heterogeneity extends not only to forms, but also to scope — systemic or idiosyncratic, isolated or simultaneous — as well as to public responses, which have themselves become increasingly fragmented.

Liquidity breaks through its execution channels

If crises are the symptom of this new regime, they need to be read across two dimensions: the form the disruption takes, and the way executable liquidity actually deteriorates.

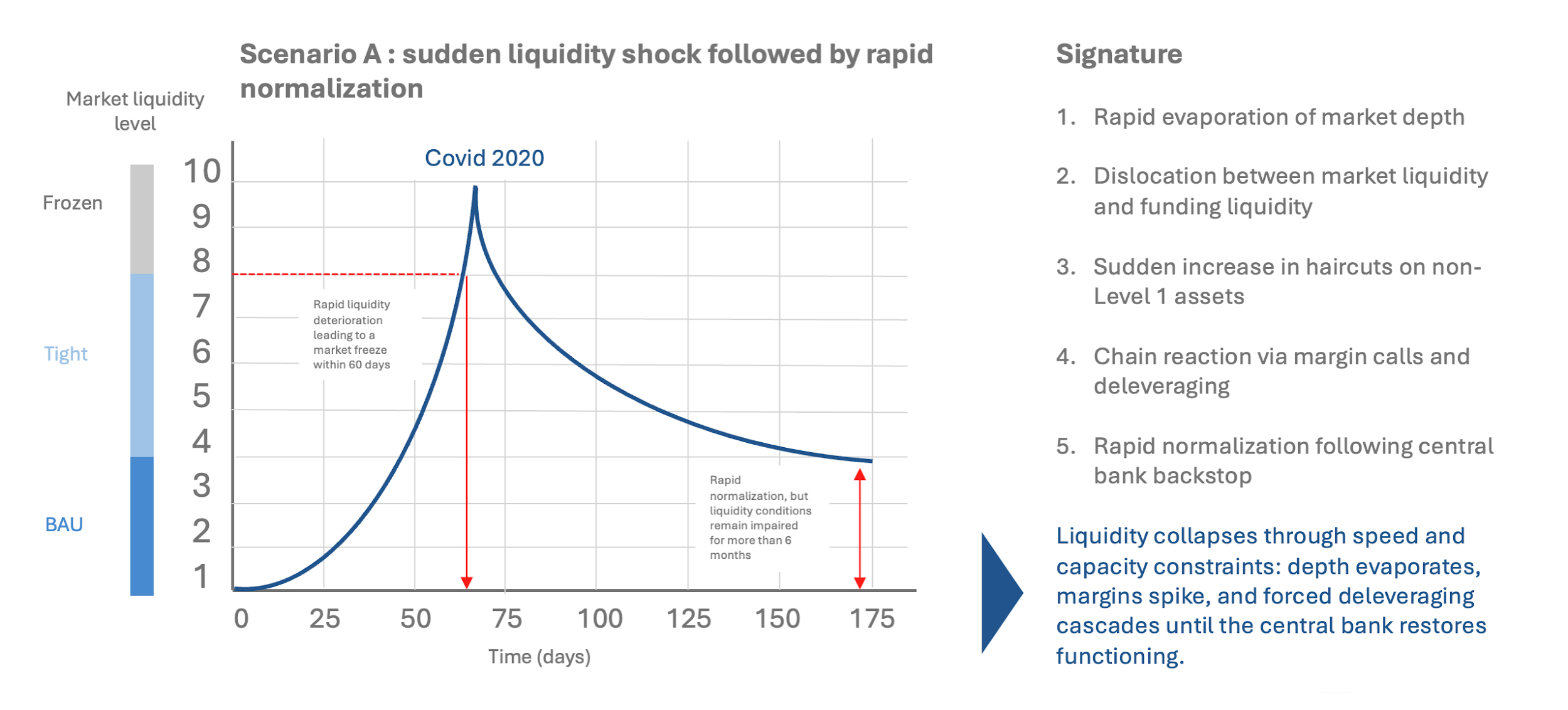

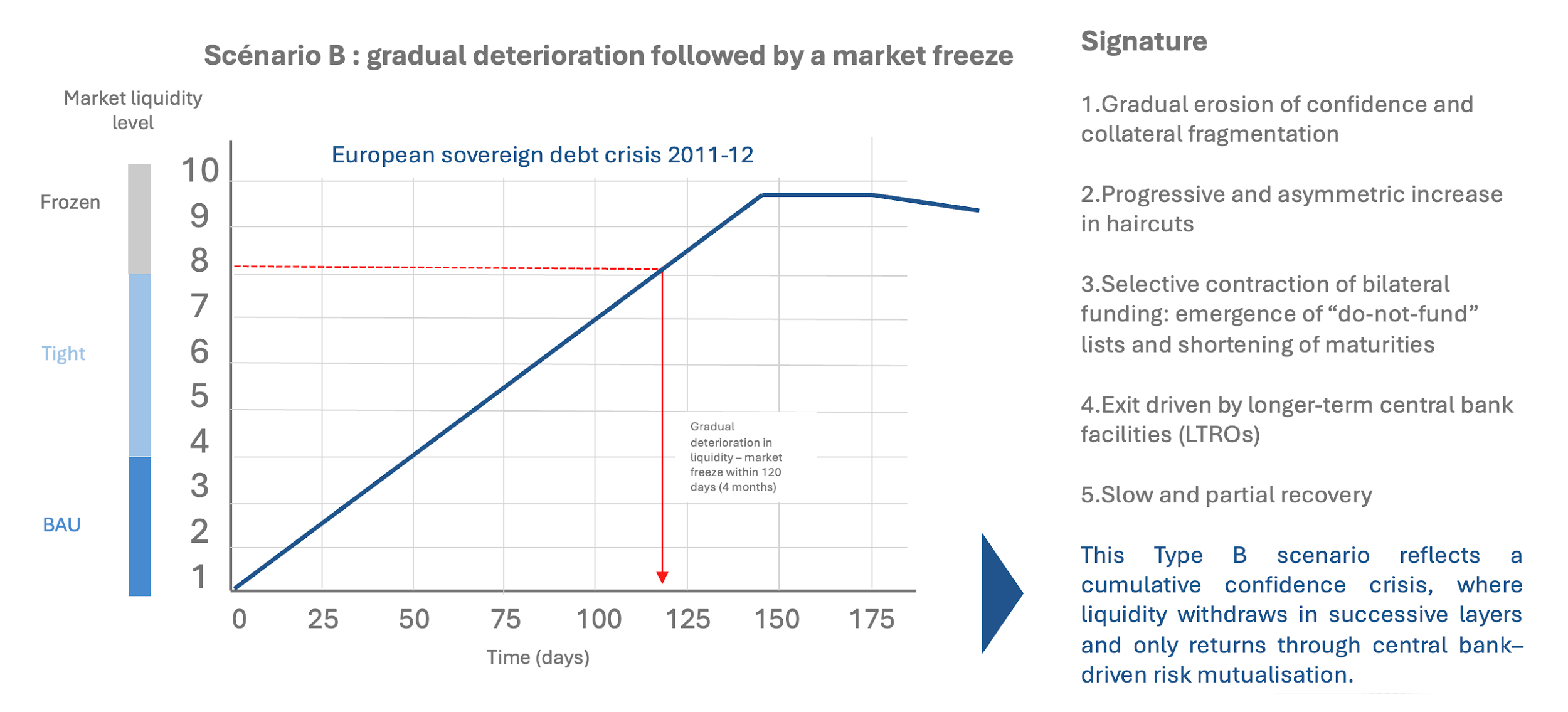

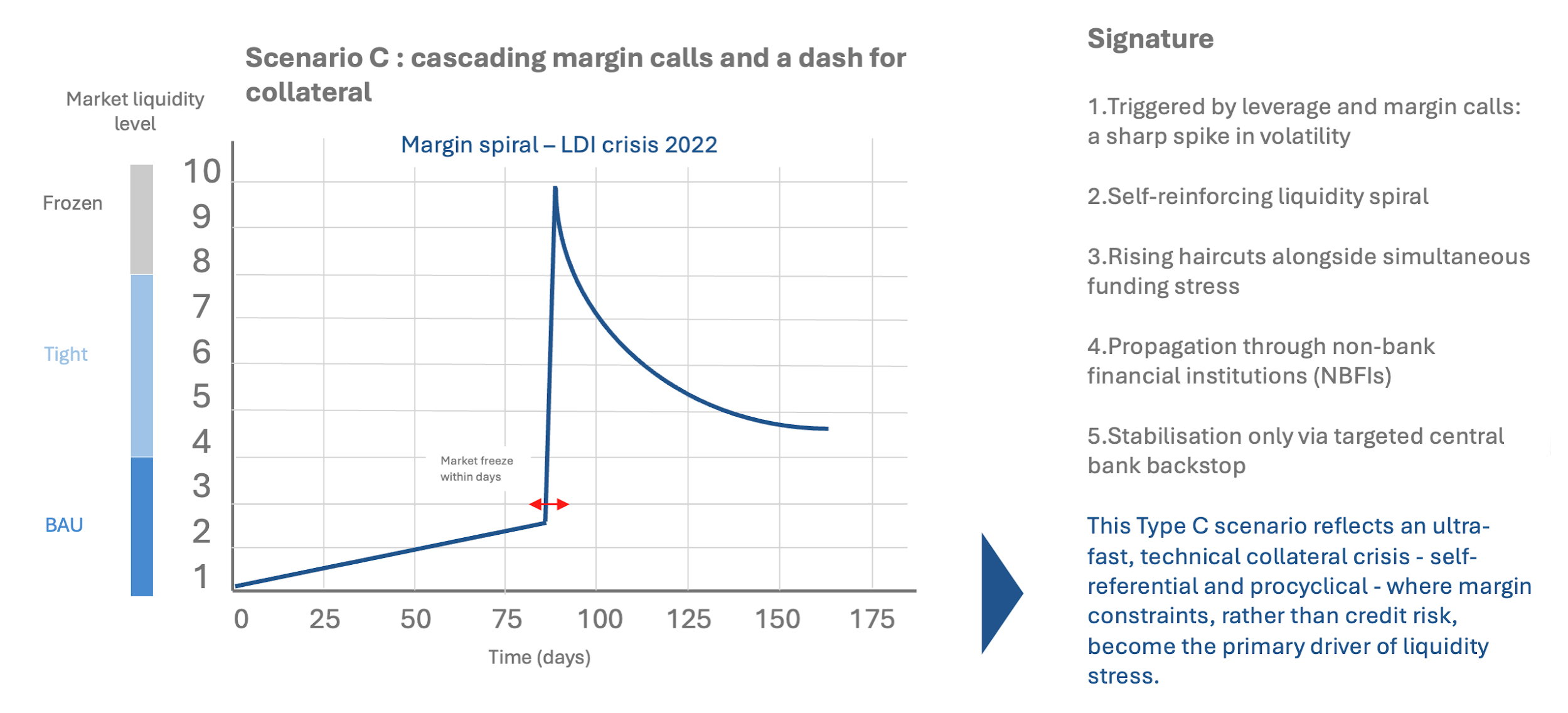

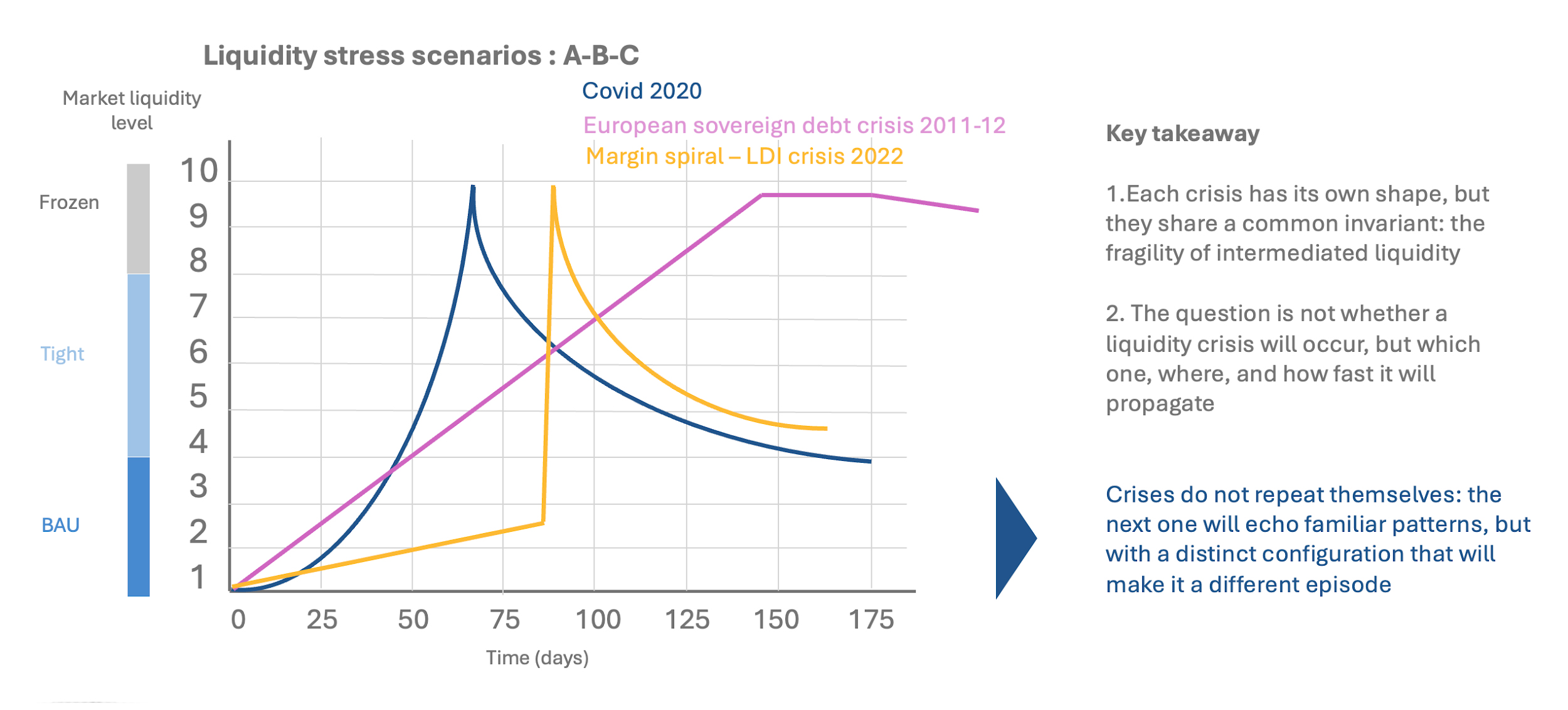

Some crises take the form of a sudden, exogenous shock, as seen during Covid in 2020 (Scenario A), where market depth evaporated instantly before being restored through public intervention. Others unfold as a slow deterioration, as in the European sovereign crisis of 2011–12 (Scenario B), where credit repricing, widening spreads, and a gradual contraction in execution capacity weaken the market without an immediate break. Others still develop through self-reinforcing dynamics, as in the UK LDI crisis in 2022 (Scenario C), where forced selling and margin calls feed on each other until market liquidity collapses. Liquidity does not disappear. It fragments.

Yet the form of the crisis alone does not explain everything. The loss of executable liquidity crystallises in purely operational elements: collateral fragmentation, where assets remain eligible but are difficult to mobilise; access failure, where infrastructure, clearing, or settlement constraints prevent mobilisation of otherwise available liquidity; or the more structural erosion of market depth, where regulatory and balance sheet constraints on key intermediaries (broker-dealers, prime brokers) durably reduce the market’s capacity to absorb flows.

The market does not lack liquidity

The next liquidity crisis is unlikely to resemble a uniform drying-up of the market. Rather, it will take the form of liquidity that remains available in theory, but becomes unusable in practice. The regime shift is already underway: liquidity no longer disappears everywhere at once; it withdraws locally, temporarily, and non-linearly.

In this context, kinetics matter more than stock. The priority, therefore, is to identify ex ante the points of blockage — the choke points — and to quantify how assets flow in both BAU and stress across each monetisation rail: bilateral repo, triparty repo, cleared repo, and central bank access. It also means mapping dependencies on specific access chains — the channels that become critical under stress. In other words, future crises will be less about a shortage of market liquidity than about the inability to transform assets into executable funding.

The centre of gravity of liquidity has shifted beyond the banking perimeter

Non-bank actors now play an increasing role in both the production and consumption of market liquidity: money market funds, hedge funds, insurers, pension funds, securitisation vehicles, financing entities, as well as crypto hedge funds and lending platforms, all contribute materially to funding dynamics.

This is not marginal. Around 15 per cent of European funding comes from these actors. Volumes have doubled between 2021 and 2025. 73 per cent of which originates outside the euro area. Concentration is extreme: 10 per cent of participants provide 80 per cent of volumes. Maturity is short: 65 per cent under seven days, 80 per cent overnight. Half of it is in US dollars, according to the ‘Financial stability risks from linkages between banks and non-banks financial intermediation sector’ report by the European Central Bank (ECB) and the European Systemic Risk Board (ESRB).

This non-banking financial institution (NBFI) liquidity is short-term, concentrated, largely offshore, and predominantly dollar-denominated; four characteristics that make it structurally unstable as a funding source. NBFI liquidity is not committed — it is rented.

Promised liquidity versus rented liquidity

By construction, bank-provided liquidity rests on a regulated balance sheet, governed by prudential requirements — such as liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) — access to central bank facilities, and implicit safety nets. This creates a continuity constraint: a bank cannot withdraw from the market instantaneously without consequence. It is committed liquidity, costly, but relatively predictable over time.

By contrast, liquidity provided by NBFIs is not anchored to a banking balance sheet, benefits from no lender of last resort, and carries no continuity obligation. It is driven by a pure arbitrage between return, risk, and liquidity, and effectively takes the form of a revocable, procyclical option.

An investment fund will fund itself in repo as long as spreads are attractive, haircuts remain acceptable, and perceived risk is stable. As soon as one of these parameters deteriorates, funding is withdrawn immediately. As a result, NBFI liquidity is rented and can disappear precisely when banks need it most.

It plays out intraday

On the banking side, liquidity has historically been managed as a stock of high-quality liquid assets (HQLA), complemented by forward projections at a 30-day horizon through regulatory stress tests. Decisions are largely taken on end-of-day, T+1, or even T+30 cycles, consistent with a balance sheet and prudential view of risk.

By contrast, NBFI liquidity operates predominantly as intraday flows. It reacts instantly to price movements, haircut adjustments, market volatility, and margin calls, and reallocates within hours, sometimes minutes.

Modern liquidity stress is therefore a crisis of speed and synchronisation. In this context, a bank may be fully compliant with LCR requirements, solvent, and well-capitalised, yet operationally illiquid if NBFI liquidity sources withdraw abruptly.

Procyclical and ungoverned haircuts

Within banks, liquidity parameters are largely governed by internal and regulatory frameworks, with relatively stable haircuts set ex ante and overseen by defined functions (ALM, risk, treasury). By contrast, NBFI liquidity is governed by private, heterogeneous, and evolving rules over which banks have no control. Haircuts are endogenous, uncoordinated, and inherently procyclical — moving with markets, not against them. These decisions are unilateral and non-negotiable: they are imposed on banks without any buffering mechanism.

NBFIs do not fund banks as entities; they fund specific collateral, at a given price and at a specific point in time. The case of US Treasuries is illustrative: widely regarded as a safe asset, they nevertheless experience rising haircuts when market volatility increases, mechanically reducing repo funding capacity precisely when liquidity demand intensifies.

Siloed organisations facing a systemic risk

The breaking point is primarily organisational. Liquidity execution remains structured in silos, while risk has shifted to the ecosystem level. Within most banks, each function operates with its own legitimate framework: Treasury manages available cash, ALM optimises regulatory ratios, risk sets limits and stress tests, and the repo desk serves clients, maximises P&L, and sources funding at the lowest cost. Each optimises within its perimeter, but based on a partial view.

What is often missing is the ability to orchestrate the dynamic interactions that now link market participants — particularly NBFIs — collateral, margin calls, and infrastructures. Liquidity no longer flows simply between bank balance sheets; it is co-produced, transformed, and sometimes blocked within a chain where each link depends on the others. Banks manage stock; the market operates in flows.

In this context, seemingly basic questions remain unanswered: who actually holds the cash in stress? Who owns and can mobilise the collateral? Who effectively sets haircuts, and according to what logic? And above all, how quickly can liquidity deteriorate or disappear? Today, very few institutions actively manage the decisive intraday metrics: time-to-cash, time-to-margin, time-to-substitution. This is precisely where modern liquidity fragility lies.

When stress hits, these are no longer theoretical considerations but immediate trade-offs: do you roll positions or allow funding to fail, post collateral or preserve optionality, access central bank liquidity or remain in the market? In practice, very few institutions structure these decisions explicitly. They are neither clearly articulated nor prioritised, and their cost is rarely explicitly acknowledged. This is a critical blind spot: in the face of private, volatile, and non-cooperative liquidity, the absence of explicit trade-offs is not just a gap, it is a loss of control. Put simply, you are exposed, and you do not know it. In stress, liquidity is not scarce — it is unusable.

In this regime, liquidity does not protect. It exposes

NBFI liquidity is not a marginal phenomenon, nor a substitute for bank liquidity. It is a major but conditional, procyclical, and revocable source of funding, which requires centralised, intraday, execution-focused management.

Figure 1

Figure 2

Figure 3

Figure 4

The price paid for liquidity density in BAU is an increasing dependence on actors with no obligation to provide continuity in stress, quite the opposite. Liquidity therefore remains a promise, and becomes non-executable the moment private liquidity ceases to cooperate. This is not insurance. It is conditional liquidity — and it breaks precisely when it needs to be executed.

The liquidity regime has changed; recent crises have made that clear. Their defining feature is heterogeneity: the message is constant, the path is not. Liquidity no longer fades in a gradual, readable way — it gaps, withdraws in blocks, fragments, and reconfigures itself across channels that do not necessarily align.

What was once treated as a stable stock to protect now operates under a different logic: an execution capacity — reversible, conditional, and prone to seize up under uncontrolled margin calls, widening spreads, or collapsing roll-over rates. Liquidity no longer fails as a stock; it fails in execution.

The prevailing analytical framework now rests on an untenable fiction: that a liquidity crisis is a rare, systemic event, primarily driven by a lack of volume, and sufficiently homogeneous to be captured by a handful of prudential metrics. Recent episodes have invalidated this view.

Shocks can be exogenous, endogenous, or structural. Breaking points may emerge in markets, balance sheets, collateral, confidence, or geopolitics. Stress then propagates through spreads, haircuts, eligibility, infrastructure constraints, withdrawal behaviour, or deleveraging loops. Crucially, time dynamics diverge sharply: some crises strike suddenly, others erode the market gradually, while others accelerate through self-reinforcing feedback loops. This heterogeneity extends not only to forms, but also to scope — systemic or idiosyncratic, isolated or simultaneous — as well as to public responses, which have themselves become increasingly fragmented.

Liquidity breaks through its execution channels

If crises are the symptom of this new regime, they need to be read across two dimensions: the form the disruption takes, and the way executable liquidity actually deteriorates.

Some crises take the form of a sudden, exogenous shock, as seen during Covid in 2020 (Scenario A), where market depth evaporated instantly before being restored through public intervention. Others unfold as a slow deterioration, as in the European sovereign crisis of 2011–12 (Scenario B), where credit repricing, widening spreads, and a gradual contraction in execution capacity weaken the market without an immediate break. Others still develop through self-reinforcing dynamics, as in the UK LDI crisis in 2022 (Scenario C), where forced selling and margin calls feed on each other until market liquidity collapses. Liquidity does not disappear. It fragments.

Yet the form of the crisis alone does not explain everything. The loss of executable liquidity crystallises in purely operational elements: collateral fragmentation, where assets remain eligible but are difficult to mobilise; access failure, where infrastructure, clearing, or settlement constraints prevent mobilisation of otherwise available liquidity; or the more structural erosion of market depth, where regulatory and balance sheet constraints on key intermediaries (broker-dealers, prime brokers) durably reduce the market’s capacity to absorb flows.

The market does not lack liquidity

The next liquidity crisis is unlikely to resemble a uniform drying-up of the market. Rather, it will take the form of liquidity that remains available in theory, but becomes unusable in practice. The regime shift is already underway: liquidity no longer disappears everywhere at once; it withdraws locally, temporarily, and non-linearly.

In this context, kinetics matter more than stock. The priority, therefore, is to identify ex ante the points of blockage — the choke points — and to quantify how assets flow in both BAU and stress across each monetisation rail: bilateral repo, triparty repo, cleared repo, and central bank access. It also means mapping dependencies on specific access chains — the channels that become critical under stress. In other words, future crises will be less about a shortage of market liquidity than about the inability to transform assets into executable funding.

The centre of gravity of liquidity has shifted beyond the banking perimeter

Non-bank actors now play an increasing role in both the production and consumption of market liquidity: money market funds, hedge funds, insurers, pension funds, securitisation vehicles, financing entities, as well as crypto hedge funds and lending platforms, all contribute materially to funding dynamics.

This is not marginal. Around 15 per cent of European funding comes from these actors. Volumes have doubled between 2021 and 2025. 73 per cent of which originates outside the euro area. Concentration is extreme: 10 per cent of participants provide 80 per cent of volumes. Maturity is short: 65 per cent under seven days, 80 per cent overnight. Half of it is in US dollars, according to the ‘Financial stability risks from linkages between banks and non-banks financial intermediation sector’ report by the European Central Bank (ECB) and the European Systemic Risk Board (ESRB).

This non-banking financial institution (NBFI) liquidity is short-term, concentrated, largely offshore, and predominantly dollar-denominated; four characteristics that make it structurally unstable as a funding source. NBFI liquidity is not committed — it is rented.

Promised liquidity versus rented liquidity

By construction, bank-provided liquidity rests on a regulated balance sheet, governed by prudential requirements — such as liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) — access to central bank facilities, and implicit safety nets. This creates a continuity constraint: a bank cannot withdraw from the market instantaneously without consequence. It is committed liquidity, costly, but relatively predictable over time.

By contrast, liquidity provided by NBFIs is not anchored to a banking balance sheet, benefits from no lender of last resort, and carries no continuity obligation. It is driven by a pure arbitrage between return, risk, and liquidity, and effectively takes the form of a revocable, procyclical option.

An investment fund will fund itself in repo as long as spreads are attractive, haircuts remain acceptable, and perceived risk is stable. As soon as one of these parameters deteriorates, funding is withdrawn immediately. As a result, NBFI liquidity is rented and can disappear precisely when banks need it most.

It plays out intraday

On the banking side, liquidity has historically been managed as a stock of high-quality liquid assets (HQLA), complemented by forward projections at a 30-day horizon through regulatory stress tests. Decisions are largely taken on end-of-day, T+1, or even T+30 cycles, consistent with a balance sheet and prudential view of risk.

By contrast, NBFI liquidity operates predominantly as intraday flows. It reacts instantly to price movements, haircut adjustments, market volatility, and margin calls, and reallocates within hours, sometimes minutes.

Modern liquidity stress is therefore a crisis of speed and synchronisation. In this context, a bank may be fully compliant with LCR requirements, solvent, and well-capitalised, yet operationally illiquid if NBFI liquidity sources withdraw abruptly.

Procyclical and ungoverned haircuts

Within banks, liquidity parameters are largely governed by internal and regulatory frameworks, with relatively stable haircuts set ex ante and overseen by defined functions (ALM, risk, treasury). By contrast, NBFI liquidity is governed by private, heterogeneous, and evolving rules over which banks have no control. Haircuts are endogenous, uncoordinated, and inherently procyclical — moving with markets, not against them. These decisions are unilateral and non-negotiable: they are imposed on banks without any buffering mechanism.

NBFIs do not fund banks as entities; they fund specific collateral, at a given price and at a specific point in time. The case of US Treasuries is illustrative: widely regarded as a safe asset, they nevertheless experience rising haircuts when market volatility increases, mechanically reducing repo funding capacity precisely when liquidity demand intensifies.

Siloed organisations facing a systemic risk

The breaking point is primarily organisational. Liquidity execution remains structured in silos, while risk has shifted to the ecosystem level. Within most banks, each function operates with its own legitimate framework: Treasury manages available cash, ALM optimises regulatory ratios, risk sets limits and stress tests, and the repo desk serves clients, maximises P&L, and sources funding at the lowest cost. Each optimises within its perimeter, but based on a partial view.

What is often missing is the ability to orchestrate the dynamic interactions that now link market participants — particularly NBFIs — collateral, margin calls, and infrastructures. Liquidity no longer flows simply between bank balance sheets; it is co-produced, transformed, and sometimes blocked within a chain where each link depends on the others. Banks manage stock; the market operates in flows.

In this context, seemingly basic questions remain unanswered: who actually holds the cash in stress? Who owns and can mobilise the collateral? Who effectively sets haircuts, and according to what logic? And above all, how quickly can liquidity deteriorate or disappear? Today, very few institutions actively manage the decisive intraday metrics: time-to-cash, time-to-margin, time-to-substitution. This is precisely where modern liquidity fragility lies.

When stress hits, these are no longer theoretical considerations but immediate trade-offs: do you roll positions or allow funding to fail, post collateral or preserve optionality, access central bank liquidity or remain in the market? In practice, very few institutions structure these decisions explicitly. They are neither clearly articulated nor prioritised, and their cost is rarely explicitly acknowledged. This is a critical blind spot: in the face of private, volatile, and non-cooperative liquidity, the absence of explicit trade-offs is not just a gap, it is a loss of control. Put simply, you are exposed, and you do not know it. In stress, liquidity is not scarce — it is unusable.

In this regime, liquidity does not protect. It exposes

NBFI liquidity is not a marginal phenomenon, nor a substitute for bank liquidity. It is a major but conditional, procyclical, and revocable source of funding, which requires centralised, intraday, execution-focused management.

Figure 1

Figure 2

Figure 3

Figure 4

The price paid for liquidity density in BAU is an increasing dependence on actors with no obligation to provide continuity in stress, quite the opposite. Liquidity therefore remains a promise, and becomes non-executable the moment private liquidity ceases to cooperate. This is not insurance. It is conditional liquidity — and it breaks precisely when it needs to be executed.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times