Initial margin for non-cleared derivatives: The end of the journey?

14 April 2026

David Beatrix, head of OTC and Collateral Services, Securities Services at BNP Paribas, provides an overview of the Uncleared Margin Rules and the latest evolutions of the IM model

Image: David Beatrix

Image: David Beatrix

From 1 September 2016 until September 2022, the Uncleared Margin Rules (UMR) were phased in, requiring each year an increasing number of market participants to exchange initial margins on their non–cleared derivative transactions.

However, due to the threshold effect of these rules, many firms are still not affected by them. Does it mean that those firms are not affected by initial margin concerns?

Reminder on the initial margin rules

Since UMR came into force, any firm whose aggregate average notional amount (AANA) of non-centrally cleared OTC derivatives exceeds €8?billion — calculated at consolidated group level — must exchange initial margins (IM). Every OTC derivative position including physically settled FX forwards and swaps is counted in the AANA calculation. The AANA is assessed annually (as of the last business day of the previous March, April, and May for the compliance date of the following January) and reaching the threshold requires each firm to activate IM exchange processes and controls.

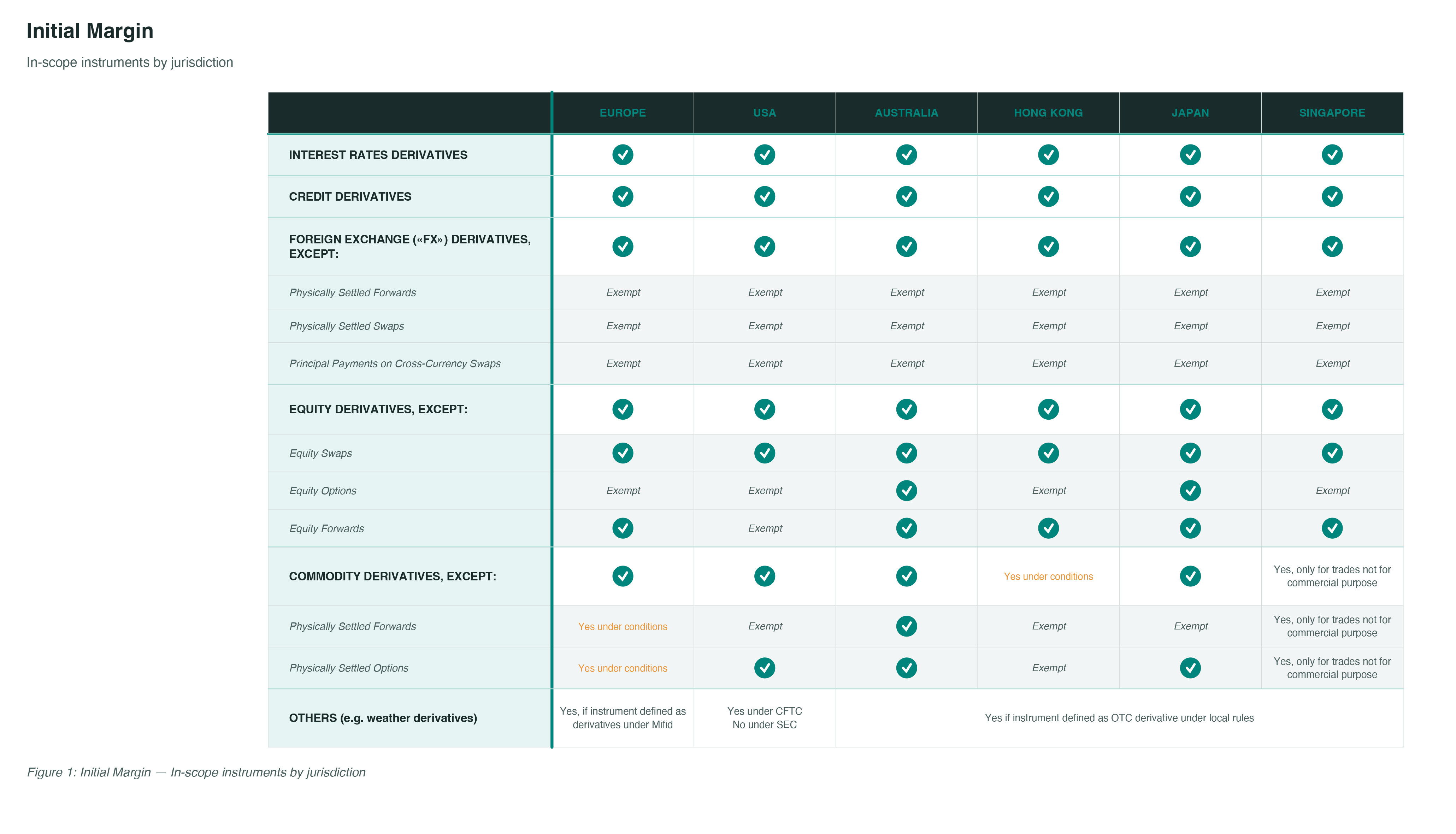

UMR has been transposed in the EU, US, Japan, Australia, Hong?Kong, Singapore, and other jurisdictions, with a strong extraterritorial effect that pulls most cross-border transactions with third country entities into scope. The instrument list is broadly consistent worldwide, excluding physically settled FX forwards, FX swaps, and the exchange of principal on cross-currency swaps, while certain carve-outs remain, e.g. equity-option exemptions in the US and lately the EU and Hong Kong.

Initial margins may be calculated using a regulator approved table-based Grid or an internal model, most commonly the International Swaps and Derivatives Association (ISDA) Standard Initial Margin Model (SIMM) with a back testing obligation. The industry is moving toward a single framework to simplify approvals and reduce disputes between participants. They are subject to a two-way exchange principle (each party posts and receives at the same time), a bankruptcy-remote obligation in terms of margins safekeeping (implying custodial segregation) and among other things, a possible relief if margins stay under a €50 million threshold.

Moreover, as part of the ISDA SIMM Governance Framework, the ISDA?SIMM Remediation Annex, published in March 2023, has set out a principle to perform back testing for portfolios above a €25?million threshold regardless of whether the portfolios are already subject to IM exchanges or not.

Complying with those rules is resource intensive, involves trading, risk, legal, middle and back office, IT, custodians, and market platforms, and normally takes several months. Firms can either build an in-house solution or enlist a service provider such as BNP?Paribas for end-to-end implementation.

Which initial margin calculation method?

The Grid method is simple as it considers only the trades notional, maturity, and net-to-gross parameters. It has the beauty of simplicity but does not consider the netting of risks inside a portfolio with a given counterparty so — except in particular situations — it will usually exhibit higher amounts than the SIMM.

Meanwhile, SIMM is more difficult to implement, maintain, and implies more complex analysis when disputes arise, however it allows netting of market risks for positions executed with the same counterparty (e.g. payer versus receiver swaps), so it reflects a more accurate picture for risk-neutral portfolios.

Despite a massive adoption of SIMM, the grid method remains an option in some relationships between banks and buy side firms, with some agreements combining the two methodologies (SIMM and Grid) depending on instrument types.

There are multiple reasons:

• Implementing SIMM can take time for certain types of instruments. Grid can be an alternative to comply quickly with the rules.

• The regulator may prescribe to use the Grid method for specific instruments where they estimate that a specific risk is not sufficiently considered by SIMM.

• Grid can lead to lower IM amounts in particular cases. As the costs involved with financing posted collateral come into play, this is an important criterion especially when collateral received cannot be reused.

For example, for a six-month bond forward with an underlying bond maturity above 10 years, the difference between Grid and SIMM can be significant. With a 40-year underlying bond maturity, the difference is about 13 per cent of the notional. Under SIMM, a longer time-to-maturity implies higher rate sensitivities therefore a higher SIMM amount, whereas Grid is capped after a certain time-to-maturity.

As a result, directional rate portfolios with long maturities — typical of insurance or pension portfolios — may in some cases exhibit lower IM amounts with Grid compared to SIMM.

When the regulation does not prescribe the use of a method, a firm can opt for the different methods listed in the Credit Support Annex (CSA) signed with its counterparty.

Initial margin threshold monitoring: Buying more time

A relief mechanism has been put in place to take into consideration the complexity of implementation for firms with low trading activity.

In April 2020, the Basel Committee on Banking Supervision (BCBS) stated in its ‘Margin requirements for non-centrally cleared derivatives’ paper:

“The requirements could impose some unnecessary operational costs on smaller entities that pose no significant systemic risk to the system and would not be expected to be bound by the initial margin requirements, in particular, in light of the provided threshold amount of €50 million.”

As always, the devil is in the detail. This €50 million threshold is the maximum threshold a firm can set with another trading relationship — both firms should consider this amount at consolidated group level. Therefore, for institutions with multiple entities, themselves in trading relationships with several branches/subsidiaries of a bank, a significant part of the preparatory work (and maintenance thereafter, acknowledging developments and creation of entities) is to map and allocate the appropriate threshold amount to each relationship, function of the expected trading activity post compliance date, the risk profile of the transactions, and the capacity of that entity to fund eligible collateral. Finally, for the same relationship, it could also be the case that these thresholds are set in an asymmetric way between the pledger and pledgee directions.

In light of that, if, for a given trading relationship, the uncleared OTC derivatives portfolio in-scope, i.e. having all its trades executed after compliance date, has its IM amounts under the threshold (€50 million or lower depending on the allocation mechanism described previously), it is then exempt of IM postings until it reaches this threshold. Firms under the threshold are not expected to have the specific documentation, custodial, or operational processes related to IM.

This, however, is only supposed to grant more time for firms and custodians to prepare for full IM compliance. Once this threshold is exceeded, firms are expected to start posting and collecting, and have all required documentation and processes in place. Therefore, precise monitoring of the thresholds is crucial.

Latest evolutions of the IM model

The latest update confirms that the biannual recalibration schedule is now fully adopted, ensuring the SIMM model stays aligned with evolving market conditions. This regular, market-driven recalibration — most recently applied in December?2025 (SIMM?v2.8?+?2506) — eliminates the previous short-fall risk by keeping model parameters consistently in step with current market dynamics.

On?3?July?2023, the EBA — responsible for overseeing Initial Margin Model Validation (IMMV) — published the final draft of the Regulatory Technical Standard (RTS) on IMMV. The RTS implements the risk-mitigation rules for non-cleared OTC derivatives contained in Article?11(15) of EMIR?(2012/648) and sets out the governance, back-testing, and documentation requirements that market participants must meet, establishing a uniform supervisory review process.

With EMIR?3.0 coming into effect at the end of December?2024, every firm exchanging IM must submit a request for IM model validation to its National Competent Authority.

The first trigger for this obligation was the recalibration of the ISDA?SIMM model on?the 7?July?2025, which constituted a ‘model change’ under EMIR?3.0. Consequently, firms were required to provide the information outlined in the EBA’s Opinion. In November?2025, the EBA issued a reminder press release, urging firms to comply before the next scheduled recalibration on?7?December?2025. Failing to submit the information to the competent authority may prevent the future validation of the model for IM calculation.

How BNP Paribas can help

At BNP Paribas, we have been supporting clients on their compliance journey since 2016 when the first obligations entered into force. We can provide a full suite of services ranging from IM calculation, exposure management, and pledge management via our triparty collateral service.

To help our clients prepare for the compliance work, we also developed a threshold monitoring service allowing them to monitor their IM levels against pre-defined IM exchange thresholds. This allows them to keep trading even though their IM framework is not fully in place.

We can help clients anticipate their funding needs and identify the most efficient trading counterparties through our pre-trade initial-margin (IM) simulation tool. This solution, available on our NeoLink portal, allows clients to visualise the IM impact of simulated trades to a number of selected counterparties, factoring the portfolio already in position with each of them, with the option to choose between Grid or SIMM. The solution is available to front-office teams and risk managers, enabling them to optimise the counterparty selection before trade execution.

We continue to support clients in the complex regulatory and market evolutions surrounding initial margins, in an integrated manner within our wider set of OTC and collateral services, and develop new solutions to facilitate their compliance processes.

However, due to the threshold effect of these rules, many firms are still not affected by them. Does it mean that those firms are not affected by initial margin concerns?

Reminder on the initial margin rules

Since UMR came into force, any firm whose aggregate average notional amount (AANA) of non-centrally cleared OTC derivatives exceeds €8?billion — calculated at consolidated group level — must exchange initial margins (IM). Every OTC derivative position including physically settled FX forwards and swaps is counted in the AANA calculation. The AANA is assessed annually (as of the last business day of the previous March, April, and May for the compliance date of the following January) and reaching the threshold requires each firm to activate IM exchange processes and controls.

UMR has been transposed in the EU, US, Japan, Australia, Hong?Kong, Singapore, and other jurisdictions, with a strong extraterritorial effect that pulls most cross-border transactions with third country entities into scope. The instrument list is broadly consistent worldwide, excluding physically settled FX forwards, FX swaps, and the exchange of principal on cross-currency swaps, while certain carve-outs remain, e.g. equity-option exemptions in the US and lately the EU and Hong Kong.

Initial margins may be calculated using a regulator approved table-based Grid or an internal model, most commonly the International Swaps and Derivatives Association (ISDA) Standard Initial Margin Model (SIMM) with a back testing obligation. The industry is moving toward a single framework to simplify approvals and reduce disputes between participants. They are subject to a two-way exchange principle (each party posts and receives at the same time), a bankruptcy-remote obligation in terms of margins safekeeping (implying custodial segregation) and among other things, a possible relief if margins stay under a €50 million threshold.

Moreover, as part of the ISDA SIMM Governance Framework, the ISDA?SIMM Remediation Annex, published in March 2023, has set out a principle to perform back testing for portfolios above a €25?million threshold regardless of whether the portfolios are already subject to IM exchanges or not.

Complying with those rules is resource intensive, involves trading, risk, legal, middle and back office, IT, custodians, and market platforms, and normally takes several months. Firms can either build an in-house solution or enlist a service provider such as BNP?Paribas for end-to-end implementation.

Which initial margin calculation method?

The Grid method is simple as it considers only the trades notional, maturity, and net-to-gross parameters. It has the beauty of simplicity but does not consider the netting of risks inside a portfolio with a given counterparty so — except in particular situations — it will usually exhibit higher amounts than the SIMM.

Meanwhile, SIMM is more difficult to implement, maintain, and implies more complex analysis when disputes arise, however it allows netting of market risks for positions executed with the same counterparty (e.g. payer versus receiver swaps), so it reflects a more accurate picture for risk-neutral portfolios.

Despite a massive adoption of SIMM, the grid method remains an option in some relationships between banks and buy side firms, with some agreements combining the two methodologies (SIMM and Grid) depending on instrument types.

There are multiple reasons:

• Implementing SIMM can take time for certain types of instruments. Grid can be an alternative to comply quickly with the rules.

• The regulator may prescribe to use the Grid method for specific instruments where they estimate that a specific risk is not sufficiently considered by SIMM.

• Grid can lead to lower IM amounts in particular cases. As the costs involved with financing posted collateral come into play, this is an important criterion especially when collateral received cannot be reused.

For example, for a six-month bond forward with an underlying bond maturity above 10 years, the difference between Grid and SIMM can be significant. With a 40-year underlying bond maturity, the difference is about 13 per cent of the notional. Under SIMM, a longer time-to-maturity implies higher rate sensitivities therefore a higher SIMM amount, whereas Grid is capped after a certain time-to-maturity.

As a result, directional rate portfolios with long maturities — typical of insurance or pension portfolios — may in some cases exhibit lower IM amounts with Grid compared to SIMM.

When the regulation does not prescribe the use of a method, a firm can opt for the different methods listed in the Credit Support Annex (CSA) signed with its counterparty.

Initial margin threshold monitoring: Buying more time

A relief mechanism has been put in place to take into consideration the complexity of implementation for firms with low trading activity.

In April 2020, the Basel Committee on Banking Supervision (BCBS) stated in its ‘Margin requirements for non-centrally cleared derivatives’ paper:

“The requirements could impose some unnecessary operational costs on smaller entities that pose no significant systemic risk to the system and would not be expected to be bound by the initial margin requirements, in particular, in light of the provided threshold amount of €50 million.”

As always, the devil is in the detail. This €50 million threshold is the maximum threshold a firm can set with another trading relationship — both firms should consider this amount at consolidated group level. Therefore, for institutions with multiple entities, themselves in trading relationships with several branches/subsidiaries of a bank, a significant part of the preparatory work (and maintenance thereafter, acknowledging developments and creation of entities) is to map and allocate the appropriate threshold amount to each relationship, function of the expected trading activity post compliance date, the risk profile of the transactions, and the capacity of that entity to fund eligible collateral. Finally, for the same relationship, it could also be the case that these thresholds are set in an asymmetric way between the pledger and pledgee directions.

In light of that, if, for a given trading relationship, the uncleared OTC derivatives portfolio in-scope, i.e. having all its trades executed after compliance date, has its IM amounts under the threshold (€50 million or lower depending on the allocation mechanism described previously), it is then exempt of IM postings until it reaches this threshold. Firms under the threshold are not expected to have the specific documentation, custodial, or operational processes related to IM.

This, however, is only supposed to grant more time for firms and custodians to prepare for full IM compliance. Once this threshold is exceeded, firms are expected to start posting and collecting, and have all required documentation and processes in place. Therefore, precise monitoring of the thresholds is crucial.

Latest evolutions of the IM model

The latest update confirms that the biannual recalibration schedule is now fully adopted, ensuring the SIMM model stays aligned with evolving market conditions. This regular, market-driven recalibration — most recently applied in December?2025 (SIMM?v2.8?+?2506) — eliminates the previous short-fall risk by keeping model parameters consistently in step with current market dynamics.

On?3?July?2023, the EBA — responsible for overseeing Initial Margin Model Validation (IMMV) — published the final draft of the Regulatory Technical Standard (RTS) on IMMV. The RTS implements the risk-mitigation rules for non-cleared OTC derivatives contained in Article?11(15) of EMIR?(2012/648) and sets out the governance, back-testing, and documentation requirements that market participants must meet, establishing a uniform supervisory review process.

With EMIR?3.0 coming into effect at the end of December?2024, every firm exchanging IM must submit a request for IM model validation to its National Competent Authority.

The first trigger for this obligation was the recalibration of the ISDA?SIMM model on?the 7?July?2025, which constituted a ‘model change’ under EMIR?3.0. Consequently, firms were required to provide the information outlined in the EBA’s Opinion. In November?2025, the EBA issued a reminder press release, urging firms to comply before the next scheduled recalibration on?7?December?2025. Failing to submit the information to the competent authority may prevent the future validation of the model for IM calculation.

How BNP Paribas can help

At BNP Paribas, we have been supporting clients on their compliance journey since 2016 when the first obligations entered into force. We can provide a full suite of services ranging from IM calculation, exposure management, and pledge management via our triparty collateral service.

To help our clients prepare for the compliance work, we also developed a threshold monitoring service allowing them to monitor their IM levels against pre-defined IM exchange thresholds. This allows them to keep trading even though their IM framework is not fully in place.

We can help clients anticipate their funding needs and identify the most efficient trading counterparties through our pre-trade initial-margin (IM) simulation tool. This solution, available on our NeoLink portal, allows clients to visualise the IM impact of simulated trades to a number of selected counterparties, factoring the portfolio already in position with each of them, with the option to choose between Grid or SIMM. The solution is available to front-office teams and risk managers, enabling them to optimise the counterparty selection before trade execution.

We continue to support clients in the complex regulatory and market evolutions surrounding initial margins, in an integrated manner within our wider set of OTC and collateral services, and develop new solutions to facilitate their compliance processes.

NO FEE, NO RISK

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

100% ON RETURNS If you invest in only one securities finance news source this year, make sure it is your free subscription to Securities Finance Times

.jpg)